The information in this brief is intended for educational use only.

This brief provides a summary of the CHOICES Learning Collaborative Partnership simulation model of a potential reduction in the Mississippi (MS) state child care licensing regulations’ current limit for daily non-educational screen time in child care. The limit would decrease from 60 minutes a day to 30 minutes a week.

The Issue

Over the past three decades, more and more people have developed obesity.1 Today, nearly nine percent of 2-5 year olds have obesity.2 Now labeled as an epidemic, health care costs for treating obesity-related health conditions such as heart disease and diabetes were $147 billion in 2008.3 While multiple strategies are needed to reverse the epidemic, emerging prevention strategies directed at children show great promise for addressing the epidemic.4 A large body of evidence shows that limiting time watching non-educational television helps kids grow up at a healthy weight.

In Mississippi, approximately 35% of 2-5 year olds attend a licensed child care program, either a center or a family daycare home.5 Licensed programs can offer healthy, nurturing environments for children, and this policy can support programs in creating a healthier screen time environment.

About the Policy to Help Licensing Care Programs Reduce Screen Time

The policy to limit screen time in child care settings to 30 minutes per week is based on national policy recommendations from pediatricians and child care and public health experts.6 Requiring the policy change through licensing regulations would reach a large number of child care programs. The policy change would also help support children’s development of healthy screen use habits.

Comparing Costs and Outcomes

CHOICES cost-effectiveness analysis compared the costs and outcomes of modifying the existing MS licensing regulations regarding screen time for child care providers over 10 years with costs and outcomes associated with not modifying the regulations. The approach assumes that 55% of licensed programs would comply with the regulation change.

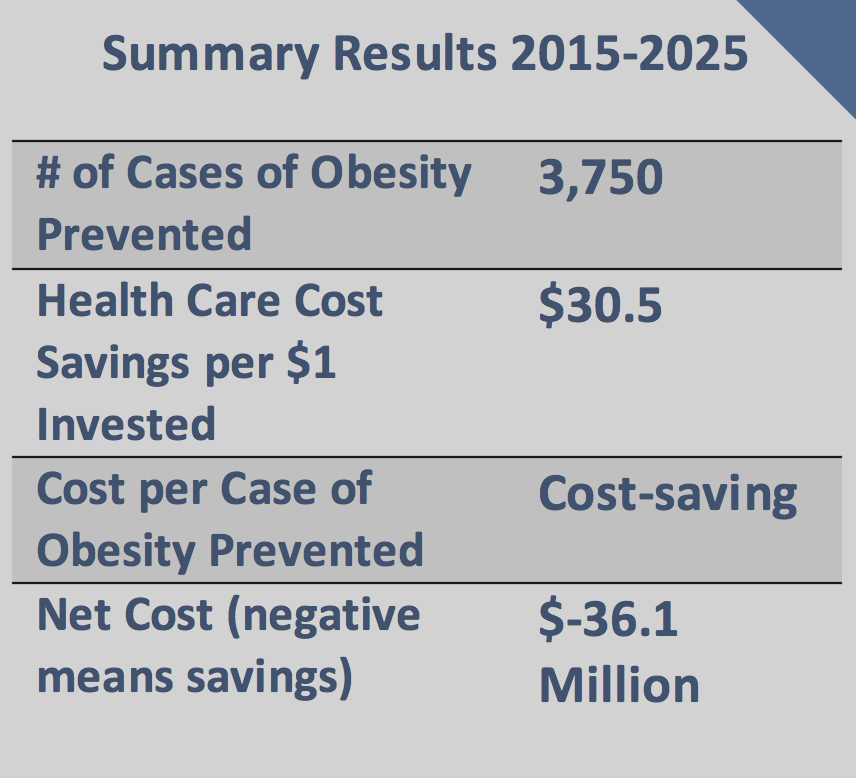

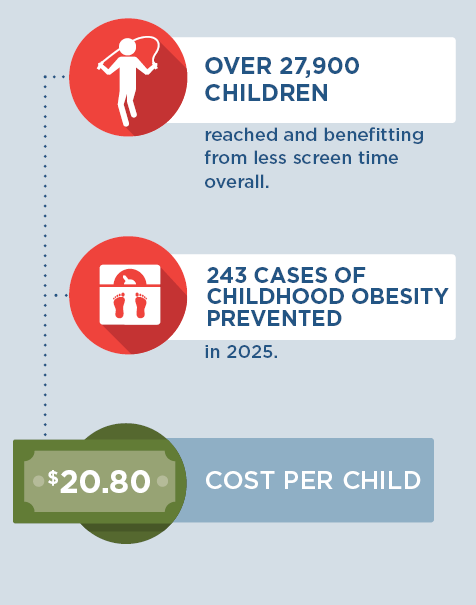

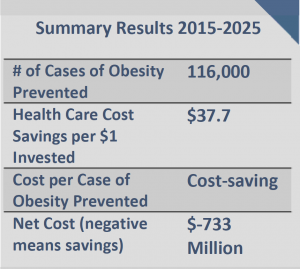

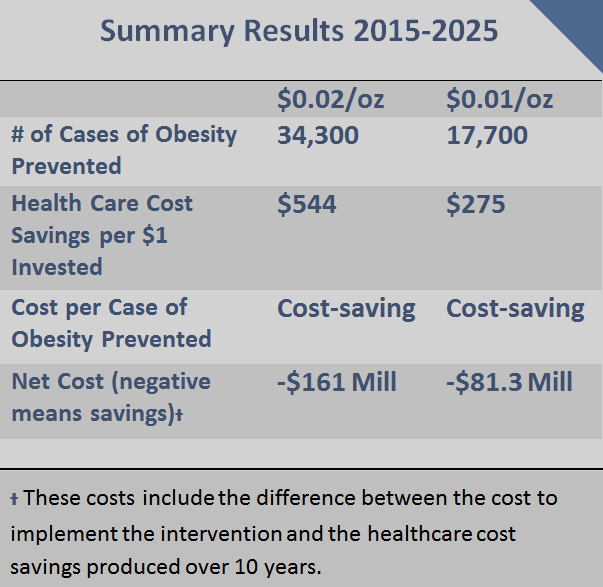

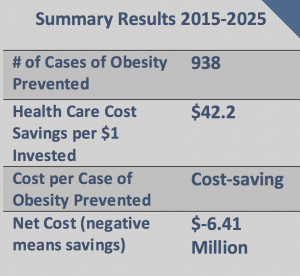

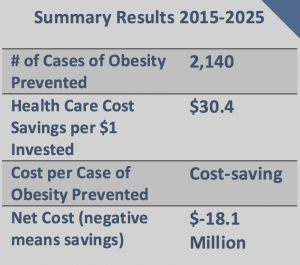

Implementing screen time reduction programs throughout MS child care is an investment in the future. By the end of 2025: |

Conclusions and Implications

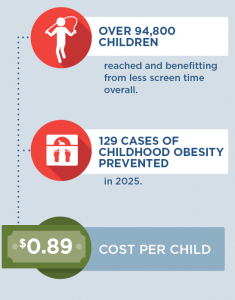

Every child deserves a healthy start in life. This includes ensuring that all kids in child care have opportunities to be healthy, no matter where they live or where they go for child care. A state-level initiative to limit non-educational screen time in child care settings could prevent 129 cases of childhood obesity in 2025 and ensure healthier child care environments for over 94,800 children.

What’s more, this is all done at a bargain – less than $1 per child annually. For every $1.00 spent on implementing this screen time strategy, we would save $0.62 in health care costs. These results reinforce the importance of investing in prevention efforts, relative to other treatment interventions, to reduce the prevalence of obesity. Shortchanging prevention efforts can lead to more costly and complicated treatment options in the future, whereas introducing small changes to young children can help them develop healthy habits for life.

Evidence is growing about how to help children achieve a healthy weight. Programs to reduce screen time in child care are laying the foundation for a healthier future by helping child care providers create environments that nurture healthy habits. Leaders at the federal, state, and local level should use the best available evidence to determine which evidence-based programs and policies hold the most promise to help children grow up at a healthy weight.

References

- Flegal, K.M., Kruszon-Moran, D., Carroll, M.D., Fryar, C.D., Ogden, C.L. (2016). Trends in Obesity Among Adults in the United States, 2005 to 2014. JAMA, 315(21), 2284-91.

- Ogden, C. L., Carroll, M. D., Lawman, H. G., Fryar, C. D., Kruszon-Moran, D., Kit, B. K., & Flegal, K. M. (2016). Trends in obesity prevalence among children and adolescents in the United States, 1988-1994 through 2013–2014. JAMA, 315(21), 2292-2299.

- Finkelstein EA, Trogdon JG, Cohen JW, Dietz W. Annual Medical Spending Attributable To Obesity: Payer-And Service-Specific Estimates. Health Affairs. 2009;28(5).

- Gortmaker, S. L., Wang, Y. C., Long, M. W., Giles, C. M., Ward, Z. J., Barrett, J. L., …Cradock, A. L. (2015). Three interventions that reduce childhood obesity are projected to save more than they cost to implement. Health Affairs, 34(11), 1932–1939.

- Communication with Mississippi Department of Public Health Child Care Licensing Office.

- American Academy Of Pediatrics, American Public Health Association, National Resource Center for Health and Safety in Child Care and Early Education. (2011). Caring for our children: National health and safety performance standards; Guidelines for early care and education programs. 3rd edition. Elk Grove Village, IL: American Academy of Pediatrics.

Suggested Citation:Grant T, Wiggins C, Shelson S, Cradock AL, Gortmaker SL, Pipito A, Kenney EL, Giles CM. Mississippi: State Regulations to Reduce Non-Educational Screen Time for Young Children in Licensed Care {Issue Brief}. Mississippi State Department of Health, Jackson, MS, and the CHOICES Learning Collaborative Partnership at the Harvard T.H. Chan School of Public Health, Boston, MA; April, 2017. For more information, please visit www.choicesproject.org |

The design for this brief and its graphics were developed by Molly Garrone, MA and partners at Burness.

This issue brief was developed at the Harvard T.H. Chan School of Public Health in collaboration with the Mississippi State Department of Health through participation in the Childhood Obesity Intervention Cost-Effectiveness Study (CHOICES) Learning Collaborative Partnership. This brief is intended for educational use only. Funded by The JPB Foundation. Results are those of the authors and not the funders.

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.5-7 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.8,9 The Dietary Guidelines for Americans, 201510 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.11-14 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.15

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.5-7 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.8,9 The Dietary Guidelines for Americans, 201510 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.11-14 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.15

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.2-4 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.5-6 The Dietary Guidelines for Americans, 20157 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.8-11 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.12

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.2-4 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.5-6 The Dietary Guidelines for Americans, 20157 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.8-11 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.12 Impact of Tax on Price to Consumers

Impact of Tax on Price to Consumers

Background

Background

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.5-7 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.8,9 The Dietary Guidelines for Americans, 201510 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.11-14 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.15

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.5-7 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.8,9 The Dietary Guidelines for Americans, 201510 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.11-14 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.15

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.5-7 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.8,9 The Dietary Guidelines for Americans, 201510 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.11-14 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.15

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.5-7 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.8,9 The Dietary Guidelines for Americans, 201510 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.11-14 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.15

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.5-7 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.8,9 The Dietary Guidelines for Americans, 201510 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.11-14 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.15

SSBs include all beverages with added caloric sweeteners. The modeled excise tax does not apply to 100% juice, milk products, or artificially-sweetened beverages. Although SSB consumption has declined in recent years, children and adults in the U.S. consume twice as many calories from SSBs compared to 30 years ago.5-7 Randomized trials and longitudinal studies have linked SSB consumption to excess weight gain, diabetes, and cardiovascular disease. Consumption of SSBs increases the risk of chronic diseases through its impact on BMI and other mechanisms.8,9 The Dietary Guidelines for Americans, 201510 recommends that individuals reduce SSB intake in order to manage their body weight. Drawing on the success of tobacco taxation and decades of economic research, public health experts have called for higher taxes on SSBs and documented their likely impact.11-14 In 2009, the IOM recommended that local governments implement tax strategies to reduce consumption of “calorie-dense, nutrient-poor foods,” emphasizing SSBs as an apt target for taxation.15